Getting a small business loan is an integral part of many small businesses to start up or grow. The most common SBA loans offered for small businesses are 7a and 504 loans. The terms of loans may seem confusing and small business owners may not understand which one they need or qualify for. In this article, we will break down the major differences between the two loan programs and which might be right for your small business.

Difference #1: Eligible Business size

Each type of SBA loan has business size requirements that may impact your eligibility. Eligibility for 7a loans is determined mainly by industry. For example retail, service or agriculture businesses' sales must not exceed the range of $750,000 - $33.5 million.For 504 loans a business’ net worth cannot exceed $15 million. Meanwhile, the average net profit (after taxes) over 2 consecutive years cannot exceed $5 million.

Difference #2: Program Requirements

The program requirements for a 7a and 504 loans are almost the same where the business owner needs to occupy at least 51% of an existing building or will occupy at least 60% for new construction.The only main difference is that all assets purchased with a 7a loan must be used for the direct benefit of the business. Meanwhile, equipment purchased with 504 loans must have a minimum of a 10-year economic life.

Difference #3: Use

The third difference we need to cover is the purpose you would need either a 504 or 7a loan. Generally speaking, a 7a is the most popular and is a multipurpose loan the SBA offers. It can be used for a whole host of business finance needs from starting to purchasing a business or growing a business. The 7a loan can also be used to help with buying equipment, working capital, purchasing inventory, or leaseholder improvements.The 504 is almost completely real estate-related like purchasing land for new construction or purchasing a building. The 504 loans can also finance building expansion or improvements and larger equipment purchases that 7a loans can’t cover.

Difference #4: Loan Amount

The next difference is the amount of money a business gets, which is significant. The 7a loan ranges from a minimum of $50,000 up to $5 million to cover the general-purpose needs for most small businesses.504 loans have a larger range for the loan amount from $125,000 up to $20 million for the specific range of real estate-related or the larger equipment purchases that I mentioned earlier.

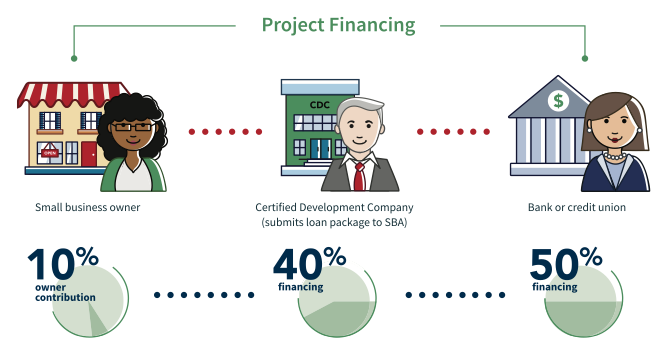

Difference #5: Loan Structure

Loan structures for 7a and 504 loans are very different. 7a loan structures are flexible and are dependent on the amount of risk but, generally have a down payment of at least 10% of the loan amount but often 20%-30%. With 504 loans, the structure looks very different.The loan is structured with 3 entities: the business owner, a bank, and a Certified Development Company (CDC).

The CDC is the primary lender in this process and handles the loan package. This will make up 40% of the total loan amount in a first mortgage. The second mortgage is supported by the SBA through a commercial bank loan and makes up 50% of the loan amount.

The final 10% will be the small business contribution and in certain circumstances such as startup (under 2 years) or special properties, may require a 20% contribution.

Difference #6: Loan Term Length

When it comes to loan term length, the differences are primarily based on the use of the funds for a 7a or 504 Loan.For example, a 7a loan that is used for the working capital range is typically a 5-7 year term. If you are looking to purchase equipment or acquire a business the loan term expands up to 10 years and up to 25 years for real estate-related purchases.

504 terms are more simplified since they cover fewer types of purchases. For example, equipment purchases are 10-year terms, while real estate-related purchases are still 25 years like the 7a.

Difference #7: Interest Rates

SBA loan programs are known for having some of the lowest rates for small business owners. 7a loans generally have higher variable rates in the range of 5.5% - 9.5%, based on the situation.

Differences #8: Collateral

Collateral for both 7a and 504 loans are fairly different with only 1 notable similarity: they require personal guarantees from principals with at least 20% ownership. Otherwise, 7a loans must have collateral for the full loan amount and the collateral can include real estate equity (both residential and investment).504 loans are very different in where the project assets or properties that are being financed can be used as collateral. This means the assets can be repossessed and sold through foreclosure the business be unable to make payments on the loan.

Difference #9: Fees

Each of these loans does come with fees associated with the process and you should be aware of how they can grow according to the type of loan you want to pursue. For the most part, fees associated with the 7a and 504 can be financed in each loan.With 7a loans there is a 0.25% surcharge on the loan over $1 million. If you decide to pair a 7a loan with a 504 loan the additional fees will vary depending on the size of the loan amounts.

With 504 loans, since there are two lenders there are two sources of fees: with the bank, loan fees are negotiated for 50% of the loan amount. On the CDC side, there is a servicing fee (2% of the loan amount) allowed by the SBA and a legal review fee.

Conclusion

The SBA 7a and 504 loans are powerful tools to start and build small businesses. You as a small business now have the information you need to determine which loan may be right for you and the considerations many small business owners are concerned with: collateral, interest rates, and fees. If you need more help with applying for an SBA loan contact your local SBDC and speak with a business consultant for free.Let us know which SBA you are interested in and what would you use it for? Throw them down in the comments below.

Funded in part through a Cooperative Agreement with the U.S. Small Business Administration. All opinions, conclusions, and/or recommendations expressed herein are those of the author(s) and do not necessarily reflect the views of the SBA.

Comments

Post a Comment